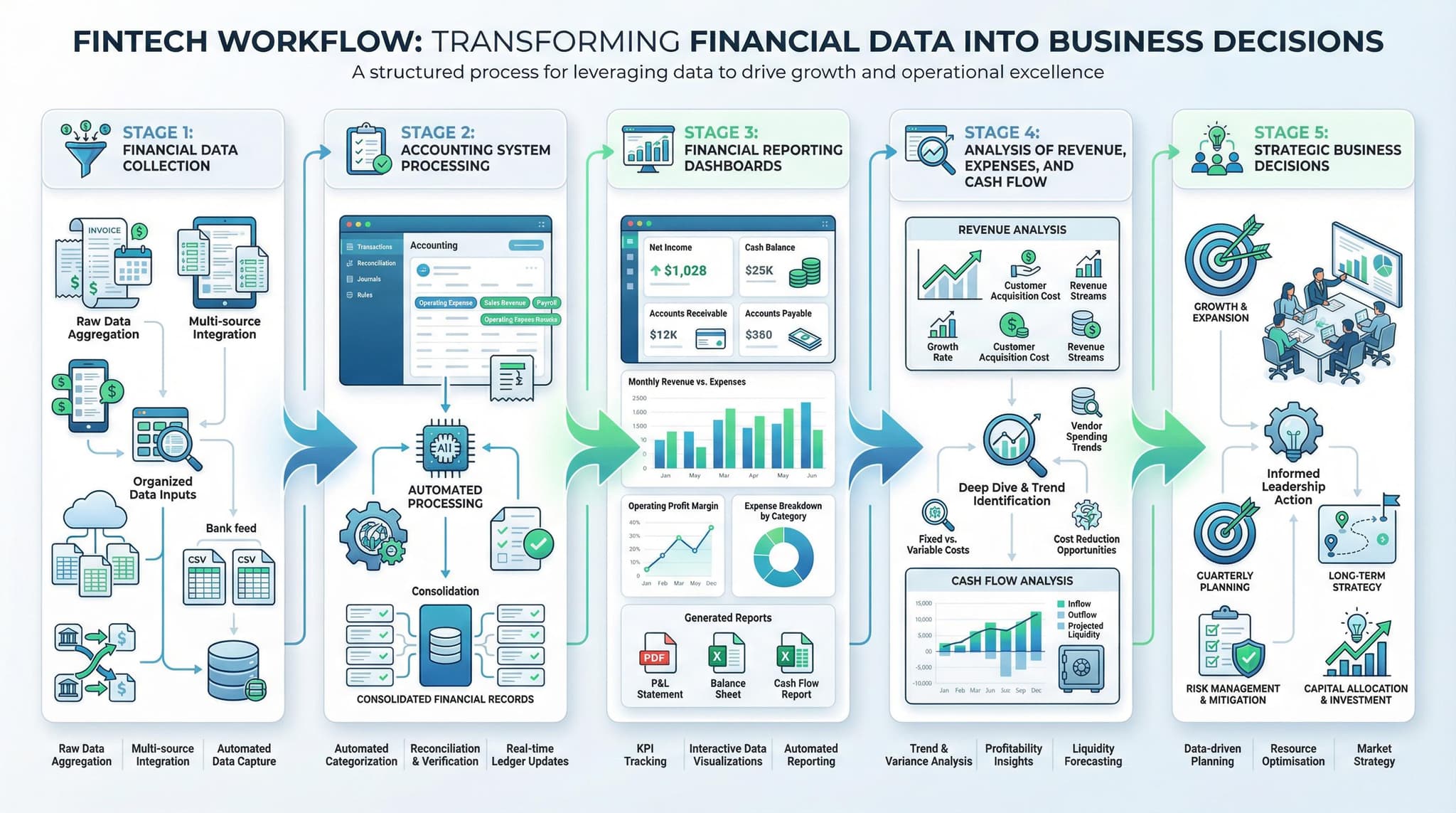

Financial Reporting: Turning Data into Decisions for UK SME Leaders

A board-ready framework for KPI reporting, variance analysis, and decision-making from live finance data.

Financial Reporting: Turning Data into Decisions for UK SME Leaders

For many UK SMEs, financial reporting still arrives too late, says too little, or sits too far away from decision-making. The business produces a profit and loss report, glances at the bank balance, files VAT, and moves on. But strong reporting is not about generating more numbers. It is about converting financial data into operating judgment — faster, clearer, and with enough context for leaders to act before issues become expensive.

The best SME leaders do not use reporting simply to describe the past. They use it to control the next few weeks and shape the next few quarters. That means turning accounts data into working-capital visibility, cash risk awareness, margin understanding, and prioritised action. In other words, reporting should not end with “what happened?” It should answer “what matters now?” and “what should we do next?”

This article sets out a practical reporting blueprint for UK SME leaders. It explains what good financial reporting should include, why digital record quality matters, how to structure a reporting cadence, which reports truly drive decisions, and how to turn accounting outputs into a management discipline rather than a compliance exercise.

Why reporting matters more now

Cash pressure, variable demand, wage inflation, and tighter working-capital conditions have made financial visibility more important for SMEs than it was a few years ago. British Business Bank guidance stresses that misunderstanding cash flow can contribute to business failure, that cash is the lifeblood of any company, and that even profitable businesses can still suffer severe short-term cash flow problems while waiting to be paid. Good reporting therefore needs to do more than show profit. It must help leaders see liquidity risk early enough to respond.

At the same time, the UK tax and compliance environment is moving deeper into digital record-keeping. HMRC’s current Making Tax Digital guidance says digital records must be created and stored in software, must capture amounts, dates, and categories, and should be kept close to the transaction date so businesses have a more up-to-date view of their affairs. That direction matters beyond tax. Better digital records are the raw material of better management reporting.

In practice, this means reporting quality is now shaped upstream. If source data is late, poorly categorised, or spread across spreadsheets and inboxes, management reports will either be delayed or misleading. But if records are current and structured, financial reporting can become a real operating advantage.

What financial reporting should do for an SME leader

Many SMEs inherit a narrow idea of reporting from year-end accounts or bookkeeping routines. The finance team produces numbers; the leadership team receives them. But a useful reporting system should do four things at once: explain performance, expose risk, support planning, and trigger action.

Explain performance

Reporting should show what drove revenue, gross margin, operating spend, and profitability rather than simply presenting totals.

Expose risk

It should surface cash pressure, overdue debtors, rising costs, tax liabilities, and trends that could weaken the business if ignored.

Support planning

Reporting should help leaders forecast cash, assess working capital, and compare actual performance against expectations or budget.

Trigger action

Each report should create decisions: chase debtors, reduce spend, change pricing, adjust hiring, delay capex, or tighten collections.

If none of those things happen, the report is probably too backward-looking or too generic. The aim is not to overwhelm leaders with finance language. The aim is to make the few numbers that matter unavoidable and actionable.

The reporting stack UK SMEs actually need

SMEs do not need a huge corporate reporting pack to make better decisions. Most need a disciplined reporting stack built around a handful of outputs delivered at the right rhythm. In most businesses, that means combining current operational visibility with a clean monthly close.

| Report | Why it matters | Decision it supports |

|---|---|---|

| Profit and loss | Shows revenue, cost structure, margin, and overhead trend. | Pricing, spend control, hiring pace, profitability focus. |

| Cash flow view or forecast | Shows whether the business can fund near-term obligations. | Collections, financing, payment timing, shortfall response. |

| Aged receivables | Shows who owes money, how late they are, and where cash is stuck. | Credit control, escalation, payment terms, debtor follow-up. |

| Aged payables | Shows near-term supplier obligations and pressure on cash. | Payment prioritisation, supplier communication, liquidity planning. |

| Balance sheet review | Shows whether reported performance is supported by sound positions. | Capital discipline, debt oversight, asset and liability review. |

| Budget or forecast variance | Shows where the business is outperforming or slipping relative to plan. | Resource allocation, corrective action, updated planning assumptions. |

Cash flow is not optional

One of the biggest reporting mistakes SME leaders make is treating profit as the main health signal and cash as an afterthought. British Business Bank guidance is explicit that cash flow affects the amount of money available to fund day-to-day operations and that a sustained period of negative cash flow can make it increasingly hard to pay bills and cover expenses. It also notes that growth itself can create cash flow problems because each sale must be funded by working capital and customers often do not pay immediately.

That means cash reporting should not be confined to a bank balance check. A leader needs a view of inflows, outflows, upcoming obligations, expected collections, and the timing gap between profit recognition and actual cash arrival. Without that, the business can look healthy in the accounts and still stumble operationally.

The practical rule is simple: if a report pack does not show current cash position, forecast pressure points, and overdue customer balances, it is incomplete for decision-making purposes.

The importance of digital records and data hygiene

Reporting quality depends on record quality. HMRC’s digital-record guidance makes this very clear in practical terms: software-based records should include the amount, date, and category of income and expenses, and they should be created as close to the transaction date as possible so the business has a more up-to-date view. The guidance also warns that once digital records are created and reported, they should not be moved manually by copying and pasting between systems where digital links are required.

For SME leaders, the broader lesson is straightforward. Weak records create weak reporting. If receipts are uploaded late, invoices are miscoded, bank feeds are not reviewed, or transactions are patched in spreadsheets after the fact, management reports lose reliability. Leaders then start distrusting the numbers, which means finance stops informing decisions and reverts to a compliance role.

Clean reporting therefore begins with operating discipline: source documents captured on time, transactions categorised consistently, reconciliations done regularly, and system ownership clearly assigned. Better reports are usually the downstream result of better workflow.

The monthly reporting rhythm

Most UK SMEs do not need real-time board packs every day. But they do need a consistent rhythm. The strongest practical model is a weekly operational pulse plus a disciplined monthly reporting close.

Weekly pulse

Review bank position, collections, overdue debtors, major supplier obligations, payroll timing, and tax liabilities. This keeps cash and execution in view between formal month-end cycles.

Month-end close

Complete reconciliations, review accruals and prepayments, check payroll and tax postings, confirm debtors and creditors, and validate management accounts before they are circulated.

Monthly leadership pack

Present profit and loss, cash flow or forecast, aged receivables, aged payables, balance sheet commentary, and variance analysis with short narrative explanations.

Decision meeting

Use the pack to decide actions: collections priorities, spending controls, pricing changes, hiring decisions, stock adjustments, financing needs, and forecast updates.

The key point is that reporting should culminate in a decision meeting, not just a distribution email. If the numbers do not lead to action, the process is incomplete.

How to make reports more useful

Many SME reports fail because they are technically correct but managerially weak. They contain numbers without interpretation, movement without explanation, and totals without business context. Leaders then default back to instinct or bank balance because the report does not clearly state what is changing.

A more useful report does three things. First, it compares: this month versus last month, actual versus budget, current debtors versus prior period, forecast versus cash obligations. Second, it explains: why gross margin moved, why overheads rose, why debtor days worsened, why VAT is higher, why cash is tighter. Third, it prioritises: three to five management actions, not twenty observations.

This is especially important in SMEs because management time is limited. The reporting pack should reduce cognitive load, not increase it. Strong finance leaders therefore translate accounting data into business language: margin pressure, delayed cash, rising labour cost, slowing customer conversion, or tax exposure coming due.

From compliance reports to management reports

There is a major difference between a compliance output and a management report. Compliance reporting is designed to meet filing, bookkeeping, or statutory requirements. Management reporting is designed to improve decisions. Both matter, but they are not interchangeable.

| Type | Primary purpose | Typical weakness if used alone |

|---|---|---|

| Compliance reporting | Meet VAT, tax, payroll, bookkeeping, and statutory obligations. | Often backward-looking and not designed to drive decisions. |

| Management reporting | Support operating, commercial, and financial decisions. | Can drift from underlying accuracy if records and reconciliations are weak. |

The goal for SME leaders is to connect the two. Compliance-quality data should feed management-quality reporting. That is where digital accounting systems and structured workflows become valuable: they reduce the gap between keeping records and using them intelligently.

The questions every report should answer

A report becomes strategic when leadership knows what questions it is meant to answer. Without that discipline, reporting expands into data collection without managerial clarity.

Performance

- Did revenue grow, and if so, from volume, pricing, or customer mix?

- Did gross margin strengthen or weaken, and why?

- Which overhead categories are moving fastest?

Cash and working capital

- What cash obligations are coming due in the next 4 to 12 weeks?

- Which debtors need action now?

- Are supplier payments aligned with expected cash inflows?

Risk and control

- Are VAT, payroll, and tax liabilities visible and funded?

- Are any balances unusually high, unreconciled, or weakly supported?

- Is any key metric deteriorating repeatedly across periods?

Who owns reporting in an SME

In small businesses, reporting often falls into a grey zone between bookkeeping, accounting, and management. That ambiguity is dangerous. Someone must own the reporting calendar, the data-quality checks, the management pack, and the decision follow-up. Otherwise, reports may be generated, but they will not shape the business consistently.

In an early-stage SME, this owner may be the founder supported by an external accountant. In a more developed company, it may be a finance manager, bookkeeper, fractional FD, or controller. What matters is not title. It is accountability for turning raw data into a repeatable management process.

Leaders should also be clear that reporting ownership is not the same as decision ownership. Finance should frame the insight, but commercial, operational, and leadership teams must still act on it. Reporting creates the visibility; management creates the response.

The SME reporting blueprint

The most effective SME reporting model is lightweight but disciplined. It does not aim for corporate complexity. It aims for reliable visibility and fast action.

1. Keep records digitally and close to the transaction date

Current, categorised records create the foundation for useful reports and reduce month-end distortion.

2. Reconcile weekly, not just monthly

Bank data, debtor balances, and major liabilities should be reviewed regularly so the month-end pack is credible.

3. Build a standard monthly pack

Use the same core reports each month so movement is visible and leadership can focus on change, not format.

4. Add short commentary, not long prose

Explain what changed, why it changed, and what should happen next. Keep interpretation focused and commercial.

5. Turn the pack into a decision meeting

Every monthly report should end with agreed actions, owners, and follow-up dates.

6. Update cash forecasts continuously

British Business Bank guidance highlights the value of forecasting because it gives clarity on likely shortfalls before they become critical. That principle should sit at the heart of SME reporting.

Final perspective

Financial reporting should not feel like a finance department ritual that the rest of the business politely receives. For UK SME leaders, it should be a control system: a way to understand what is changing, where risk is building, and what the business should do before problems become harder to solve.

The strongest reporting cultures usually do not produce the biggest packs. They produce the clearest decisions. They connect good digital records to good monthly discipline, and good monthly discipline to management action on cash, margin, cost, and growth.

That is how data becomes decisions. Not by adding more spreadsheets, but by building a reporting rhythm strong enough to turn financial information into leadership judgment.