5 Common Payroll Mistakes UK Small Businesses Make and How to Fix Them Permanently

A complete payroll control framework for UK SMEs covering RTI, tax codes, pensions, and error-proof execution.

5 Common Payroll Mistakes UK Small Businesses Make and How to Fix Them Permanently

Payroll errors rarely begin as major disasters. Most start as small shortcuts — a starter added without the right paperwork, a pension contribution checked too late, an RTI submission rushed through on payday, or a payment to HMRC left until the final date. The problem for UK small businesses is that payroll mistakes rarely stay small. One incorrect pay run can affect employee trust, tax reporting, pension duties, cash flow, and compliance all at once.

That is why the smartest way to think about payroll is not as a monthly admin task but as an operating system. If the process depends on memory, last-minute effort, or one person “just knowing how it works,” errors become repeatable. If the process is structured with clear cut-offs, checklists, software controls, and named ownership, payroll becomes stable, predictable, and much easier to scale.

This guide breaks down the five payroll mistakes UK small businesses make most often, why they keep happening, what damage they cause, and how to fix them permanently. The goal is not just to help you correct payroll after something goes wrong. It is to help you redesign the process so the same issue does not happen again next month.

Why payroll mistakes repeat

Small businesses often assume payroll errors come from one-off carelessness. In reality, they usually come from recurring system weakness. If joiners are set up inconsistently, if payroll data arrives late, if pension checks are done casually, or if submissions are filed in a rush, the business has created a structure where mistakes are likely rather than accidental.

This is especially true in smaller teams where payroll sits with an office manager, bookkeeper, or director who also handles other responsibilities. The payroll process becomes heavily person-dependent. It may work most months, but it is fragile. When deadlines tighten, staff change, or HMRC notices arrive, the underlying weakness becomes visible.

The permanent fix is to reduce dependency on memory and replace it with process design. That means documented onboarding steps, pre-payroll validation, exception reporting, pension review, and a post-payroll reconciliation that confirms the numbers reported, paid, and owed all match.

At a glance

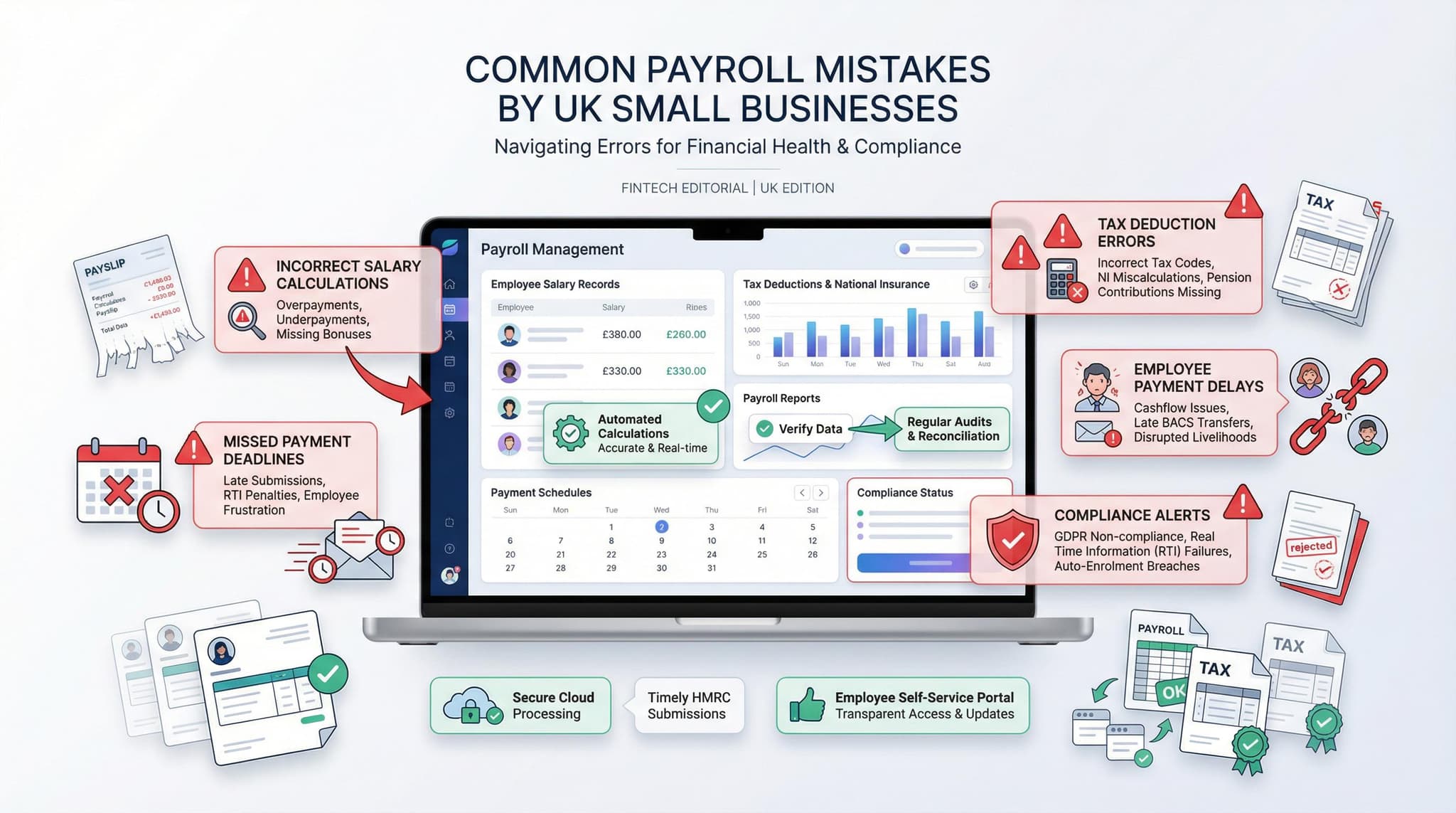

What usually goes wrong

Late RTI submissions, wrong employee setup, incorrect tax or NI treatment, pension auto-enrolment mistakes, minimum wage breaches, and late PAYE payments are the most common payroll failures in UK small businesses.

What fixes them permanently

Fixed cut-off dates, mandatory starter documentation, payroll validation checklists, pension exception reviews, minimum wage testing after deductions, and scheduled HMRC payments turn payroll into a controlled process instead of a recurring risk.

The five most common mistakes

| Mistake | What it causes | Permanent fix |

|---|---|---|

| Late or inaccurate FPS/EPS submissions | RTI penalties, incorrect PAYE records, employee tax issues, and avoidable corrections. | Use fixed payroll cut-offs, draft review, and submission sign-off before payday. |

| Poor starter and leaver setup | Wrong tax code, duplicate records, incorrect final pay, and employee record errors. | Create a mandatory joiner/leaver workflow with checklist-based setup. |

| Wrong tax code, NI category, or deduction setup | Overpayments, underpayments, HMRC corrections, and employee complaints. | Add a pre-payroll validation step for codes, NI letters, loans, and notices. |

| Auto-enrolment pension errors | Missed contributions, wrong communications, backdated corrections, and regulator risk. | Review thresholds every tax year and run pension checks every pay cycle. |

| Minimum wage and PAYE payment failures | NMW underpayment risk, late-payment penalties, and cash flow disruption. | Test pay after deductions and schedule HMRC payments before the legal deadline. |

1. Late or inaccurate RTI submissions

This is the payroll mistake that often triggers the first serious HMRC problem. Many small businesses run payroll on payday, notice something is wrong, rush the figures, and then submit the Full Payment Submission or Employer Payment Summary without a proper final check. The submission may be late, incomplete, or simply wrong.

The impact can be wider than many employers realise. Once payroll information is submitted incorrectly, the error does not stay inside the payroll file. It affects HMRC’s PAYE position, employee records, and the business’s own payroll history. Fixing it usually takes more time than doing it properly in the first place.

The permanent fix is to move payroll forward in the calendar. Set an internal cut-off date before payday. Lock the employee changes list. Run a draft payroll. Review variances against the previous period. Confirm gross pay, deductions, dates, and leavers. Then submit only after a named reviewer signs it off. Businesses that do this stop treating payroll as a race against the clock.

2. Incorrect starter and leaver processing

Joiners and leavers create a disproportionate share of payroll errors. New employees may be added without a P45, without a starter checklist, or with incomplete personal data. Leavers may be processed with the wrong leaving date, the wrong final payment, or the wrong holiday pay adjustment. Because these changes affect tax treatment and record continuity, even a small setup error can create a long trail of corrections later.

In many small businesses, this happens because no one owns the process properly. HR may not exist formally. Payroll details may arrive by email, WhatsApp, or verbal instruction. The payroll operator then fills gaps based on guesswork or urgency. That is how tax code mistakes and duplicate records happen.

The permanent fix is a strict joiner/leaver workflow. Every starter should have a standard setup pack: full legal name, address, date of birth, National Insurance number, start date, pay rate, payment frequency, P45 or starter checklist, pension status, and bank details. Every leaver should have a standard exit review: leaving date, final pay, holiday pay adjustment, deductions check, pension treatment, and confirmation that the final payroll record is correct.

3. Wrong tax code, NI category, or deduction setup

This mistake is especially common when payroll is handled by non-specialists. An employee is added quickly, the default tax code is left unchanged, the wrong NI category letter is selected, or a student loan setting is missed. The payroll still runs, which creates a false sense that everything is fine, but the deductions are already wrong from the first payslip onward.

Because these errors affect take-home pay directly, they are often discovered by employees before the employer notices them. That creates avoidable tension and damages confidence in the payroll process. It also means later corrections become more awkward because they affect both the employee and the tax position already reported.

The permanent fix is a formal pre-payroll validation step for all new employees and any employee with a status change. Before the first live pay run, review the tax code, NI category, student loan status, pension treatment, pay frequency, and any HMRC notices received. Then repeat a lighter version of this check at the start of each new tax year.

4. Pension auto-enrolment mistakes

Auto-enrolment errors are one of the most underestimated payroll risks in small businesses. Employers often assume pension deductions are automatic once the provider is connected. In reality, the process still depends on correct earnings assessment, contribution calculations, employee communication, and ongoing monitoring. Mistakes do not always show up immediately, which makes them more dangerous.

This is where many small firms get caught. They run payroll correctly from a wage perspective but fail on the pension side by using the wrong thresholds, missing an enrolment trigger, or not communicating properly with staff. The error can sit there for months and then surface later as a backdated correction issue.

The permanent fix is to build pension review into the payroll cycle itself. At the start of every tax year, review thresholds and provider settings. Each pay run, run a pension exception review: new eligible workers, opt-outs, contribution changes, maternity-related cases, and any anomalies between pensionable earnings and calculated deductions. Every three years, track re-enrolment and re-declaration as formal compliance events, not optional reminders.

5. Minimum wage breaches and late PAYE payments

Many employers think minimum wage problems only happen when they intentionally underpay staff. In reality, they often happen through technical payroll design. Deductions, salary sacrifice arrangements, unpaid working time, uniforms, and role-specific costs can all reduce effective pay below the required level even when the basic hourly rate looks acceptable on paper.

At the same time, a payroll can be calculated correctly but still create compliance pain if PAYE and National Insurance are paid late. This usually happens because the payroll itself is finalised late, cash planning is weak, or the business relies on someone remembering the payment date rather than scheduling it properly. By that point, the payroll issue has turned into both a tax and cash management problem.

The permanent fix is twofold. First, test minimum wage compliance after deductions and after any salary sacrifice arrangement, not just at the headline pay rate. Second, treat HMRC payment as part of the payroll close process rather than a separate later task. Build the payment release date into the calendar before the legal deadline so payroll cannot be “finished” until both reporting and payment are aligned.

The permanent payroll control system

Fixing payroll permanently means replacing ad hoc effort with a repeatable control framework. The simplest version of that framework works well even in a very small business.

Pre-payroll controls

- Set a payroll cut-off date for all changes, hours, bonuses, and expense inputs.

- Require complete starter and leaver documentation before changes are processed.

- Validate tax codes, NI categories, pension status, and deduction settings.

Payroll run controls

- Run draft payroll before payday rather than finalising on the day itself.

- Review net pay variances, unusual deductions, low-pay risks, and pension exceptions.

- Confirm RTI submission dates and approval responsibility before filing.

Post-payroll controls

- Reconcile payroll journal totals to the payroll reports.

- Confirm PAYE, NI, pension, and loan liabilities are scheduled for payment.

- Store reports, approvals, and corrections in a clear payroll archive.

Who should own payroll quality

Even in a small company, payroll quality needs clear ownership. That does not mean one person does everything. It means each part of the process has a named owner. One person gathers changes. One person validates setup. One person reviews the draft run. One person approves submission and payment. When nobody owns the steps, the business ends up relying on assumptions.

For very small businesses, this may be split between an office manager, an accountant, and a director. For larger SMEs, it may sit with a bookkeeper or payroll administrator supported by a finance manager. The exact structure matters less than the clarity. A defined owner for each control point is what turns payroll from a fragile routine into an operational process.

What “fixed permanently” really means

A payroll issue is not fixed permanently when you correct one payslip or submit one amended return. It is fixed permanently when the process that created the problem is redesigned. If the same conditions still exist next month — late changes, weak onboarding, no validation, rushed filing, unclear pension review, or payment dates left to memory — the error has only been patched, not solved.

Permanent payroll improvement is usually less about adding complexity and more about reducing ambiguity. Use a checklist. Set deadlines. Lock the data. Review the draft. Check the exceptions. Approve the return. Pay HMRC on schedule. These are not glamorous changes, but they are the ones that stop payroll problems from recurring.

Final perspective

Payroll mistakes are common in UK small businesses not because payroll is impossible, but because many businesses run it with informal habits rather than formal controls. The good news is that the same five mistakes tend to appear again and again, which means the fixes are also repeatable.

If your business can tighten RTI timing, standardise starter and leaver processing, validate tax and NI setup, review pensions every cycle, and build minimum wage and HMRC payment checks into the workflow, payroll becomes far more stable. That does more than reduce compliance risk. It improves employee trust, cash discipline, and operational confidence.

The real goal is not simply error-free payroll next month. It is a payroll system that keeps producing the right result even when the business gets busier, the team changes, or deadlines tighten. That is what permanent improvement looks like.