MTD for Income Tax 2026: Everything UK Business Owners Need to Know

MTD for Income Tax is a UK government initiative requiring businesses and landlords to keep digital financial records and submit tax updates to HMRC using compatible software. Starting from April 2026, many self-employed individuals and landlords above the income threshold must follow these digital reporting rules. Using MTD-compatible accounting software helps automate record-keeping, quarterly updates, and final tax submissions.

MTD for Income Tax 2026: Everything UK Business Owners Need to Know

Making Tax Digital for Income Tax becomes mandatory from 6 April 2026 for the first wave of sole traders and landlords, and it marks one of the biggest practical changes to Self Assessment in years. For affected taxpayers, compliance will move away from a single annual return-only mindset toward software-led digital record-keeping, quarterly updates, and year-end finalisation.

That sounds technical, but the real impact is operational. Businesses that already keep clean digital records will adapt more easily. Businesses that still rely on year-end catch-up, spreadsheets, and delayed bookkeeping will feel the change much more sharply.

This guide explains what starts in 2026, who is affected first, how quarterly updates work, what still happens at year-end, what exemptions matter, and how UK business owners should prepare now rather than waiting until the first filing deadline arrives.

What starts in 2026

HMRC says sole traders and landlords will need to use Making Tax Digital for Income Tax from 6 April 2026 if their qualifying income was over £50,000 in the 2024 to 2025 tax year. HMRC also says the next phase starts from 6 April 2027 for those with qualifying income over £30,000 in the 2025 to 2026 tax year, while the government has set out plans to extend the regime to those with qualifying income over £20,000 in a later phase.

The first mandatory quarterly update deadline for the 2026 start cohort is 7 August 2026. That gives affected taxpayers only a short runway between the start of the tax year and the first live deadline.

| Qualifying income test | Mandatory start date | What it means |

|---|---|---|

| Over £50,000 in 2024 to 2025 | 6 April 2026 | First mandatory group for MTD for Income Tax. |

| Over £30,000 in 2025 to 2026 | 6 April 2027 | Second mandatory group one year later. |

| Over £20,000 in 2026 to 2027 | Later legislation | Planned extension announced, but detailed commencement still needs legislation. |

Who needs to comply

HMRC says you need to use the service if you are a sole trader or landlord registered for Self Assessment, receive income from self-employment or property or both, and meet the relevant qualifying income threshold. Partnerships will also come into MTD for Income Tax later, but HMRC says the timeline for partnerships will be announced in the future.

One important point is that HMRC reviews your Self Assessment return and your qualifying income each tax year, and HMRC says it will write to taxpayers who need to start using the service by the beginning of the upcoming tax year. However, HMRC also states that if you do not receive a letter, it is still your responsibility to check whether you need to use MTD for Income Tax and prepare in time.

HMRC also says you do not need to start using the service until after you have submitted your first Self Assessment tax return, although you can sign up early if you want to prepare sooner.

What qualifying income means

The key test is qualifying income from self-employment and property, not simply salary, dividends, or total income from every source. That distinction matters because many taxpayers instinctively compare the threshold to profit or overall personal income and reach the wrong conclusion.

For most business owners, the practical takeaway is simple: if you are self-employed, receive property income, or both, you should review the relevant figures in the tax year HMRC is using for the threshold test rather than relying on rough estimates. Borderline cases should be checked carefully before April 2026.

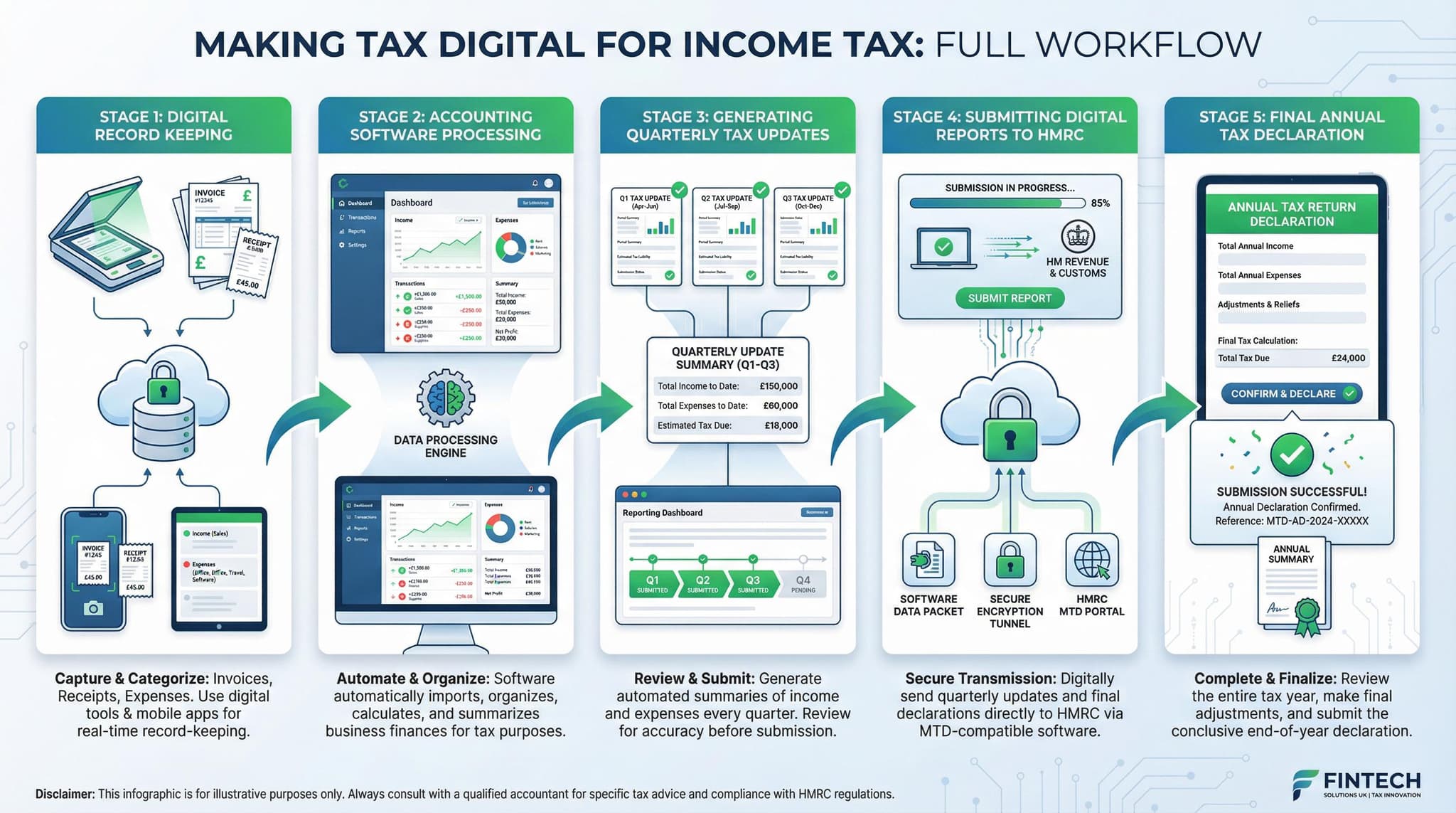

How the new system works

MTD for Income Tax is built around four core duties: keeping digital records, using compatible software, sending quarterly updates, and then finalising your tax position at year-end. Thinking in those four layers makes the regime much easier to understand than thinking of it as “more tax returns.”

Digital records

You must keep income and expense records digitally in compatible software rather than reconstructing them at year-end.

Compatible software

The software must support the MTD workflow so records and submissions can be handled digitally.

Quarterly updates

Every three months, totals for income and expense categories are sent to HMRC for each relevant self-employment or property source.

Year-end finalisation

After the tax year, the position still needs to be checked, adjusted where necessary, and finalised before the tax return is completed.

How quarterly updates work

HMRC says that every 3 months your compatible software will add together your digital records for each business to create totals for each income and expense category. Those totals are what get sent to HMRC as quarterly updates.

HMRC also says you do not need to make accounting or tax adjustments before sending a quarterly update. The updates are based on the digital records held at that point, and later corrections can be included in subsequent updates so the original quarterly update does not need to be resubmitted.

Another important detail is that HMRC will receive category totals rather than the details of every individual digital record. If you had no income and no expenses during the update period, HMRC says you still need to send the quarterly update to tell them.

Quarterly deadlines

| Standard update period | Deadline | Calendar update period | Deadline |

|---|---|---|---|

| 6 April to 5 July | 7 August | 1 April to 30 June | 7 August |

| 6 April to 5 October | 7 November | 1 April to 30 September | 7 November |

| 6 April to 5 January | 7 February | 1 April to 31 December | 7 February |

| 6 April to 5 April | 7 May | 1 April to 31 March | 7 May |

HMRC says taxpayers can use either standard update periods aligned to the tax year or calendar update periods ending on the last day of a month, depending on what best fits their accounting period. If you want to use calendar update periods, HMRC says you must select that option in your software before your first update is made for the tax year.

What still happens at year-end

One of the most common misunderstandings is that quarterly updates replace the annual final tax process. They do not. Quarterly updates are summary submissions during the year, but the tax year still has to be completed properly at the end.

HMRC says that after you have sent the final quarterly update for the tax year, you should check whether you need to make adjustments to your self-employment and property income. That means year-end work does not disappear. It simply sits on top of a more continuous digital reporting process.

In practical terms, this means taxpayers will still need good records for adjustments, reliefs, other income sources, and the final completion of their tax position. Businesses that assume quarterly reporting removes year-end discipline are likely to struggle.

Exemptions and special cases

HMRC says there are different reasons why a person may be exempt from MTD for Income Tax, including digital exclusion. If someone is exempt, they do not have to use MTD for Income Tax, but they must still continue to report income and gains through Self Assessment.

HMRC also says that if you used the SA109 supplementary page for your 2024 to 2025 tax return and expect to use it again for your next tax return, you will not need to use MTD for Income Tax before April 2027. That is an important carve-out because it means some taxpayers who otherwise appear to be in scope for April 2026 may have a later start date.

Because exemption rules can depend on circumstances, the safest approach is to check HMRC’s exemption guidance directly if your tax affairs involve residence issues, digital exclusion, trust or estate income, or other less standard reporting factors.

Penalties and the first-year soft landing

HMRC says late submission penalties may apply if you do not send quarterly updates by the relevant deadline once you are required to use the service. However, HMRC also says that for taxpayers who need to use MTD for Income Tax from 6 April 2026, it will not apply penalty points for late quarterly updates for the first 12 months.

That is helpful, but it should not be misunderstood. HMRC makes clear that you will still need to send your quarterly updates before you are able to submit your tax return, and penalty points will still apply for late tax returns. In other words, the first year is a bedding-in period for quarterly update penalties, not a free pass to ignore the new system.

What business owners should do now

1. Confirm whether you are in scope

Review your 2024 to 2025 qualifying income if you are a sole trader or landlord and check whether you cross the £50,000 threshold.

2. Choose software early

Do not wait until summer 2026. The first quarterly deadline comes quickly, so software selection and setup should happen before the tax year begins.

3. Move to digital record-keeping now

If records are still delayed, paper-heavy, or spreadsheet-led, the transition will be harder. The earlier you move to current digital records, the easier quarterly reporting becomes.

4. Decide who owns the process

Be clear whether you will manage MTD directly, your accountant will manage it, or both of you will share the workflow.

5. Build a quarterly reporting calendar

Create internal bookkeeping and review deadlines before HMRC’s filing dates so updates are not prepared at the last minute.

6. Keep year-end discipline

Quarterly reporting does not remove the need for year-end adjustments and final completion, so keep that part of the process planned and organised.

Why this matters beyond tax

MTD for Income Tax is often framed as a compliance burden, but it can also force a useful upgrade in financial discipline. Businesses that keep records digitally, review income and expense categories regularly, and work through software-led reporting usually gain better visibility over performance during the year, not just at tax time.

That does not mean the transition will be easy for everyone. For some taxpayers it will feel like a major process change. But the businesses that prepare early are much more likely to turn it into a workflow improvement rather than a recurring filing headache.

Final perspective

From April 2026, MTD for Income Tax becomes real for the first group of UK sole traders and landlords. The change is not simply that there are more deadlines. The deeper change is that tax reporting becomes digital, continuous, and software-led in a way that rewards current records and penalises year-end improvisation.

The smartest response is to prepare before the first quarterly deadline is close enough to create panic. If your business may be in scope, the right time to tidy records, choose software, and define responsibilities is now.