MTD and VAT Mastery: Building HMRC-Ready Workflows with Sage

A deep technical and operational guide to VAT control, MTD workflows, and monthly compliance confidence.

MTD and VAT Mastery: Building HMRC-Ready Workflows with Sage

Making Tax Digital for VAT has already changed the compliance baseline for UK businesses. VAT is no longer just a quarter-end form filing exercise. It is now a digital record-keeping and software workflow issue, which means the quality of your processes matters almost as much as the accuracy of your figures. For businesses using Sage, that shift creates a real advantage: VAT can move from being a stressful periodic task into a controlled, repeatable operating process built around digital records, software-led calculations, and direct submission to HMRC.

The phrase “MTD compliant” often sounds simpler than it really is. In practice, compliance depends on how records are created, where source data lives, how information moves between systems, who reviews the VAT position, and how cleanly the business can move from day-to-day transaction processing to quarter-end submission. A business can buy compliant software and still run weak workflows. It can also keep decent records and still fall short if data is moved manually in ways that break digital links. The real objective is not just software adoption. It is workflow mastery.

This guide explains how UK businesses can build HMRC-ready VAT workflows with Sage. It covers what MTD for VAT requires, what Sage does well, how to structure finance operations around digital controls, where businesses usually fail, and how to design a quarter-end process that is faster, cleaner, and more defensible under review.

Why MTD for VAT still matters

Some businesses think the real transition happened years ago and that MTD for VAT is now “done.” In reality, many businesses are only technically compliant. They file through software, but still rely on weak routines behind the scenes: late coding, spreadsheet patchwork, incomplete document capture, and quarter-end clean-up. That creates risk because MTD for VAT is not just about the submission channel. It is about digital records and digital links throughout the VAT process.

That risk matters because all VAT-registered businesses are now expected to keep digital records and submit VAT returns using compatible software. For businesses still relying heavily on spreadsheet-led or manual correction processes, the compliance issue is no longer whether they should modernise, but whether their current setup would stand up to scrutiny if questioned. The operational burden of weak VAT processes is also significant: delayed reporting, missed liabilities, poor visibility over cash flow, and increased dependence on one person to “sort it all out” every quarter.

Businesses that master MTD workflows gain more than compliance. They gain speed, cleaner controls, better tax visibility, and a more resilient finance process. That is especially important for growing SMEs where VAT becomes entangled with cash planning, debtor management, purchasing discipline, and month-end reporting.

What HMRC expects under MTD for VAT

Under Making Tax Digital for VAT, affected businesses must maintain certain records digitally and submit VAT returns using compatible software or bridging software. Where multiple programs are used, the transfer of data between them must happen through digital links rather than manual copying and re-keying. Once data has been entered into software as part of the electronic VAT account, further movement and use of that data should happen digitally. That is the core compliance logic businesses need to design around.

In practical terms, that means the VAT workflow should be built around digital transaction records, structured VAT coding, and software-led reporting. Manual intervention is not banned in every form, but the more a business depends on copy-and-paste fixes, re-keyed totals, and offline adjustments, the weaker its MTD posture becomes. MTD is therefore as much a process discipline as a technology rule.

| MTD requirement | What it means in practice | Workflow implication |

|---|---|---|

| Digital records | VAT-relevant transaction data must be kept digitally rather than reconstructed manually at the end of the quarter. | Invoices, bills, credit notes, and adjustments should enter the system in real time or near real time. |

| Compatible software | VAT returns must be submitted through commercial software that connects to HMRC. | Submission should sit inside the accounting process, not outside it. |

| Digital links | Data transfers between software components should happen digitally rather than by manual re-keying. | Avoid copy-paste VAT control models and disconnected spreadsheets wherever possible. |

| Accurate VAT return totals | The figures submitted must flow from complete and correctly coded records. | VAT code governance, review routines, and exception handling matter every week, not just at filing time. |

How Sage supports HMRC-ready VAT workflows

Sage positions Sage Accounting as MTD- and HMRC-compatible VAT software for UK small businesses. On the VAT features page, Sage says users can choose VAT rates, run reports, and submit VAT returns online in just a few clicks, with direct submission to HMRC. Sage also says its VAT accounting software is designed to simplify complex VAT returns, calculate VAT automatically, provide a monthly snapshot of the current position, and keep a record of previous VAT submissions. For many SMEs, that combination is exactly what turns VAT from a manual deadline exercise into a manageable operating process.

Sage also supports the most common VAT schemes in the UK, including Standard, Cash-based, Flat Rate, and Flat Rate Cash-based. That matters because the strongest workflow is not just about submitting on time; it is about configuring the software correctly from the start so VAT is calculated under the right rules. Businesses that use the wrong VAT setup can still produce a return, but the compliance risk sits upstream in configuration and coding.

The practical strength of Sage is that it combines day-to-day bookkeeping and quarter-end VAT handling in one environment. Bank feeds, invoices, expenses, tax codes, reporting, and submission all live together. When used properly, that reduces the amount of manual movement between systems and supports a cleaner digital trail from source transaction to VAT return.

What Sage does well

Direct VAT submission to HMRC, support for common UK VAT schemes, monthly VAT snapshots, previous submission history, and software-led VAT calculation create a strong base for compliant small-business workflows.

Where businesses still need discipline

No software can fix late data capture, poor VAT coding, mixed business and personal spend, unreconciled bank data, or quarter-end panic reviews. Workflow design still determines compliance quality.

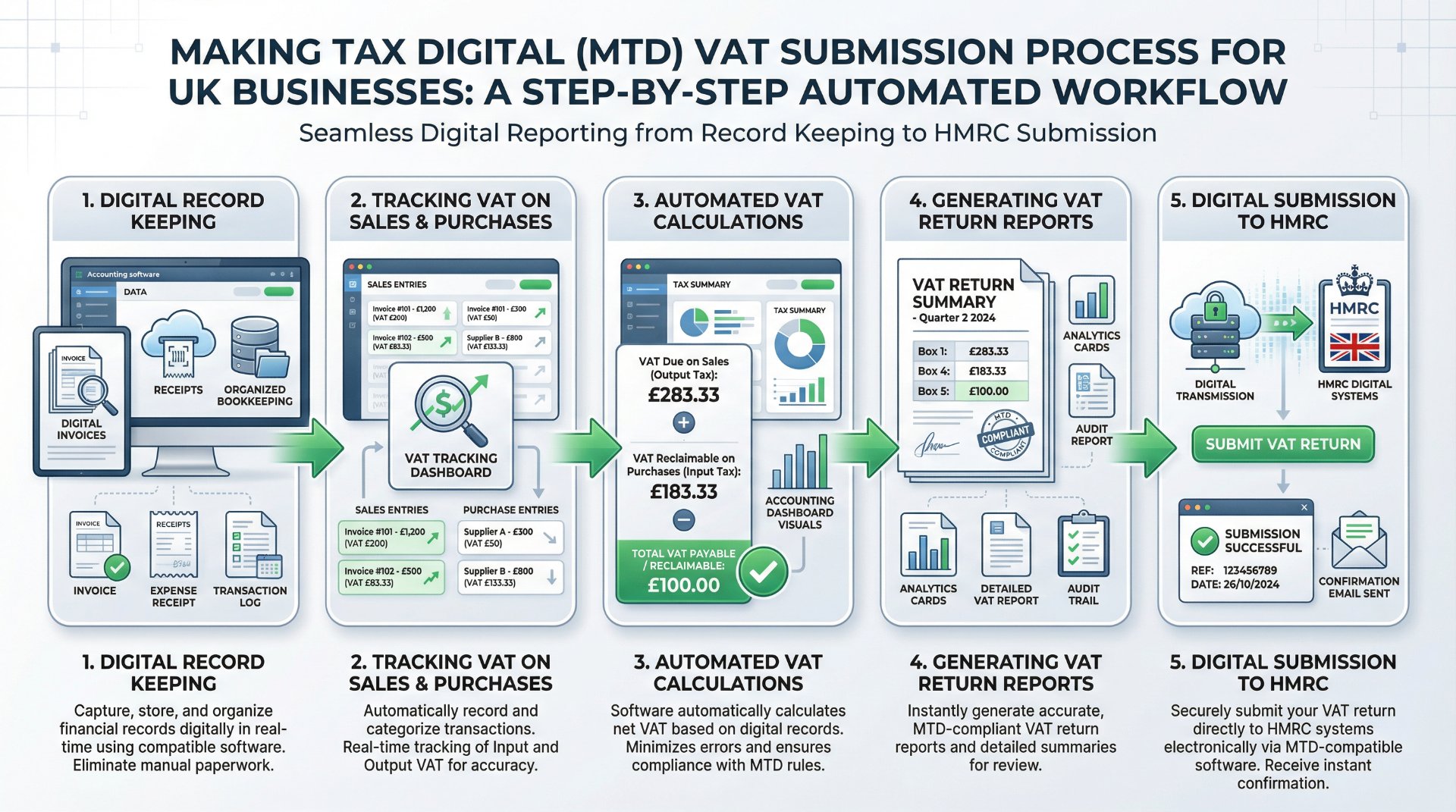

The real workflow: from transaction to VAT return

A robust MTD-ready VAT process with Sage starts long before the submission screen. It begins the moment a financial event happens — a sales invoice is raised, a supplier bill is received, an expense is incurred, or a bank transaction lands. If the source transaction is not captured properly, VAT quality is already compromised.

The next layer is classification. The business needs the right VAT code, the right transaction category, and the right supporting evidence attached or accessible. Then comes review: reconciliations, exception handling, and checks on unusual items. Only after these layers are done should the business move into VAT reporting, liability review, and submission approval.

This is why high-performing VAT workflows are not purely finance-team processes. They involve purchasing, sales admin, expense submitters, approvers, and management reviewers. Sage can hold the transaction data and reporting logic, but the business still needs a clear operating model around who captures what, who reviews what, and who signs off what.

The six-part HMRC-ready workflow blueprint

1. Capture at source

Every sales invoice, supplier bill, credit note, and expense should enter Sage as close to the transaction date as possible. This reduces missing data, improves VAT accuracy, and avoids quarter-end backlogs.

2. Standardise VAT coding

Define which VAT codes apply to recurring transaction types, suppliers, and revenue streams. The more coding decisions are standardised, the fewer quarter-end corrections are needed.

3. Reconcile continuously

Bank feeds should be active and reviewed regularly. Sales, purchase, and bank records need to stay aligned so the VAT position reflects reality rather than assumptions.

4. Run monthly VAT reviews

Do not wait until the quarter closes. Use Sage's VAT reporting and snapshots to review liability trends, exceptions, and unusual postings every month.

5. Lock down quarter-end checks

Before submission, review unreconciled items, duplicate entries, missing invoices, non-standard VAT codes, large journals, and scheme-specific treatments. This is the compliance control point.

6. Submit and archive cleanly

Submit directly to HMRC from Sage, retain the submission record, and document the internal reviewer and approval date. That creates a clean audit trail for future reference.

Where SMEs usually get VAT wrong

Most VAT problems are not software failures. They are operating failures. The first is delay: receipts uploaded late, bills entered after month-end, or sales adjustments left outside the core ledger until someone remembers them. The second is coding inconsistency: the same type of transaction gets coded differently by different people, which undermines the quality of the VAT report. The third is over-reliance on spreadsheets: totals are checked or manipulated outside the accounting system in ways that become difficult to trace and defend.

Another common weakness is treating VAT as a quarterly event instead of a continuous process. Businesses often look at the VAT report only when a deadline approaches, which means issues pile up silently. By the time someone reviews the position, there may be missing supplier invoices, unmatched bank lines, duplicate postings, or incorrect scheme treatments buried in the data. At that point, the process becomes reactive rather than controlled.

There is also a governance issue. In many SMEs, one person “owns VAT” informally, but nobody has formally designed the control process. That creates key-person risk. If that person is absent, the business may struggle to understand what is complete, what is pending, and what still needs to be reviewed before filing.

Designing the review layer

Submission quality improves dramatically when businesses formalise a review layer between bookkeeping and filing. The review layer should not be overly bureaucratic, but it must be real. The most effective model is a short monthly review plus a more detailed quarter-end sign-off.

| Review stage | What to check | Owner |

|---|---|---|

| Weekly | Bank feed completeness, new supplier bills, missing receipts, unusual transactions, unreconciled items. | Bookkeeper or finance admin |

| Monthly | VAT trend review, control account reasonableness, scheme application, high-value transactions, expense coding consistency. | Finance lead or external accountant |

| Quarter-end pre-close | Outstanding postings, duplicate or reversed items, journals affecting VAT, exceptions, major purchase/sales timing issues. | Finance manager / accountant |

| Submission approval | Final VAT return totals, supporting reports, payment or refund expectation, sign-off evidence, submission confirmation. | Director, finance head, or authorised reviewer |

Month-end versus quarter-end: the smarter rhythm

One of the biggest VAT workflow upgrades an SME can make is to stop thinking in quarters and start thinking in months. Quarter-end filing becomes dramatically easier when the records are already clean month by month. The goal is not to create extra work. It is to spread the work into smaller, more manageable control cycles.

A strong monthly rhythm means each month has the same core sequence: capture source documents, reconcile bank data, review VAT codes, investigate exceptions, and confirm that the VAT liability looks sensible relative to revenue and spend. By the end of the quarter, the return is then mostly a review-and-submit exercise rather than a clean-up project.

This is where Sage's reporting becomes valuable. A monthly snapshot of the VAT position gives finance teams and owners a way to track liabilities before the quarter closes. That improves both compliance readiness and cash planning, because VAT is seen as an accumulating obligation rather than a deadline surprise.

Special cases: spreadsheets, bridging, and mixed setups

Not every business operates entirely inside one accounting platform. Some still use spreadsheets for adjustments, specialist systems for billing, or separate applications for stock and expenses. HMRC's MTD logic allows multi-system environments, but the movement of data between components must happen through digital links rather than manual copy-paste re-entry. That means businesses using mixed setups need to be much more deliberate about workflow architecture.

Sage itself notes that bridging software may be useful in more complex VAT arrangements where spreadsheets need to be brought into compliance with MTD rules. However, bridging should not be treated as a permanent excuse for weak processes. In many SMEs, it is better understood as a transitional solution or a specific remedy for edge cases rather than the foundation of the whole VAT model.

The closer the business can bring its VAT records, coding, and reporting into one structured software environment, the lower the friction. Mixed setups can still be compliant, but they need more documentation, more process discipline, and clearer control over how data flows from one point to another.

Cash flow, visibility, and the business value of clean VAT workflows

VAT compliance is often discussed as if it were separate from business performance. In reality, weak VAT workflows usually signal broader finance weaknesses. Late transaction capture affects not just tax returns but also cash visibility, debtor reporting, expense control, and month-end reporting quality. The business that does not know its VAT position until the filing deadline usually also lacks a reliable current view of liabilities more broadly.

Clean workflows with Sage improve visibility because they connect the VAT process to the rest of the financial operating system. Sales flow into revenue reporting. Purchase invoices shape creditor visibility. Bank feeds support reconciliations. VAT reports become part of monthly management review rather than a side exercise. This is where compliance creates value beyond avoiding errors or penalties.

For growing businesses, that operational value compounds. Better VAT discipline usually means better bookkeeping discipline. Better bookkeeping discipline usually means better management accounts. Better management accounts usually mean faster decisions. MTD readiness, in other words, is often a proxy for finance maturity.

Who should own the process

The right ownership model depends on the size of the business. In a small owner-managed business, the bookkeeper may manage day-to-day records, the external accountant may review the VAT return, and the director may approve submission. In a larger SME, the process may sit with a finance manager supported by team members for purchases, sales, and expense capture.

What matters is clarity. There should be no ambiguity over who captures documents, who reviews VAT coding, who handles exceptions, who approves the return, and who presses submit. Without that clarity, quarter-end work tends to become diffuse and deadline-driven. With it, the business can run VAT as a standard operating process.

Choose a lightweight ownership model if you are a small business

- Bookkeeper maintains records and reconciliations weekly

- Accountant reviews VAT position monthly or quarterly

- Director approves final return before submission

- Sage serves as the shared live record for everyone involved

Choose a structured ownership model if you are a growing SME

- AP, AR, and expense capture are allocated across the finance workflow

- Finance lead owns VAT code governance and monthly review

- Controller or external adviser signs off exceptions and quarter-end adjustments

- Senior approver authorises submission and liability planning

What an HMRC-ready quarter-end looks like

An HMRC-ready quarter-end should feel calm, not improvisational. By the time the VAT return is prepared in Sage, the business should already know that bank reconciliations are current, source documents are captured, exceptions have been reviewed, and the liability looks reasonable in context. The submission itself should be one step in a control sequence, not the moment when the real work begins.

Practically, that means there should be a simple quarter-end checklist. Check for unreconciled items. Review large or unusual transactions. Confirm VAT scheme settings. Validate credit notes and adjustments. Review any manual journals. Compare the VAT position to recent periods and underlying revenue/spend activity. Then approve, submit, and archive the submission evidence.

When businesses build that rhythm into their Sage workflow, VAT becomes more predictable and less personality-dependent. That is what mastery looks like: not the absence of complexity, but a process strong enough to handle it without panic.

Final perspective

Making Tax Digital for VAT is often presented as a technology requirement, but the deeper reality is that it is a workflow standard. Businesses that treat it as a filing feature will stay only minimally compliant. Businesses that treat it as a finance operating model will gain better control, faster closes, stronger audit trails, and more reliable tax outcomes.

Sage gives UK SMEs a strong foundation for this because it combines bookkeeping, VAT calculation, reporting, and direct HMRC submission in one environment. But the real advantage comes when businesses build disciplined routines around it: digital capture, standard coding, continuous reconciliation, monthly review, and structured quarter-end approval.

That is the difference between filing VAT digitally and mastering VAT digitally. One keeps you moving. The other makes the finance function stronger.